What Is the 50/30/20 Rule? A Simple Budgeting Strategy

What Is the 50/30/20 Rule? A Simple Budgeting Strategy

Budgeting does not need to be complicated. The 50/30/20 rule is a widely used budgeting framework that helps people understand how their income may be allocated across essential costs, discretionary spending, and savings or debt reduction.

In this guide, you’ll learn what the 50/30/20 rule is, how it works, its potential advantages and limitations, and practical steps you can use if you want to try it in your own budget.

We’ll also cover situations where this framework may not suit your circumstances and outline general options people sometimes explore when managing short-term financial pressure.

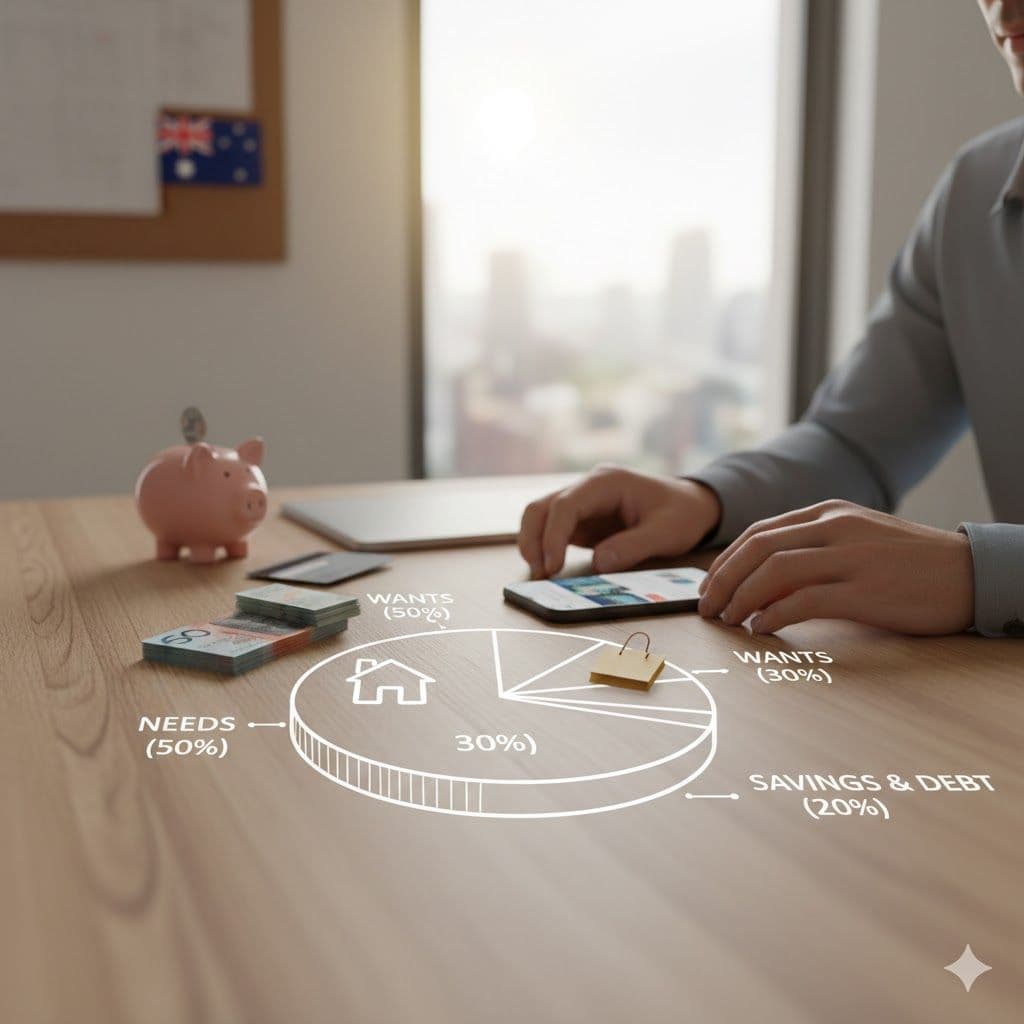

What is the 50/30/20 budgeting rule?

The 50/30/20 rule is a general budgeting framework that divides after-tax income (take-home pay) into three broad categories:

50% Needs30% Wants20% Savings and Debt Repayments

The approach was popularised by U.S. Senator Elizabeth Warren in the book All Your Worth: The Ultimate Lifetime Money Plan and is often used as a simple starting point for building budgeting habits.

Key things to know:

- It uses after-tax income, not gross income.

- It aims to balance essential living costs, discretionary spending, and progress toward savings or reducing debt.

- Many people adjust the percentages depending on their real-world expenses (for example, higher housing costs).

For more budgeting fundamentals, see:

How to do a budget: https://www.credit24.com.au/blog/how-to-do-a-budget

Breaking down the 50/30/20 rule categories

50% to Your Needs

Needs are the essential costs you generally need to pay to live and work. In Australia, these may include:

- Rent or mortgage

- Basic groceries

- Utilities (electricity, gas, water, internet, phone)

- Healthcare and insurance

- Transportation (fuel, car running costs, public transport)

- Childcare and school-related costs

- Minimum repayments on credit cards or loans

- HECS/HELP repayments

These are typically higher-priority expenses. If your “needs” exceed 50% of your income, the rule can still be used as a reference point to help identify areas where adjustments might be possible.

30% to Your Wants

Wants are discretionary expenses that can improve your lifestyle but are not strictly necessary. Examples include:

- Dining out, coffees, or takeaway

- Entertainment (movies, concerts, sporting events)

- Subscriptions and streaming services

- Hobbies and recreational activities

- Travel and weekend trips

- Non-essential shopping

- Gym memberships or classes

A simple guideline is that if an expense could be delayed or reduced without major consequences, it may fall into the “wants” category.

For tips on managing spending on a tight budget, see:

How to budget and save money on a low income: https://www.credit24.com.au/blog/how-to-budget-and-save-money-on-a-low-income

20% to Your Savings and Debt

This category focuses on building financial resilience and improving your financial position over time. It may include:

- Emergency fund contributions

- Extra repayments on loans or credit cards (above the minimum)

- Saving for a home deposit

- Investments such as shares, ETFs, or managed funds

- Education savings

- Voluntary super contributions

Many people prioritise reducing higher-interest debt while also building a small buffer for unexpected expenses.

Benefits of the 50/30/20 budgeting rule

This budgeting framework is often used because it can help you:

- Keep budgeting simple without detailed spreadsheets

- Build awareness of where your money goes

- Balance essential costs, lifestyle spending, and future goals

- Identify patterns such as rising discretionary spending

- Adjust gradually rather than changing everything at once

- Develop habits that support long-term financial literacy

Drawbacks of the 50/30/20 budget

Although useful for some households, this budgeting method may not suit everyone. Potential limitations include:

- It may not feel detailed enough if you prefer strict expense tracking

- “Needs” may exceed 50% in higher cost-of-living areas

- The 20% savings target may be difficult to reach for some incomes

- It can be harder to apply if income changes month to month

- It may not clearly account for irregular expenses such as insurance or car registration

- Some costs may sit between “needs” and “wants”

Because of this, many people treat the 50/30/20 rule as a guide rather than a strict rule.

How to create a 50/30/20 budget plan

Step 1: Determine your after-tax income

Start by calculating your monthly take-home income. This may include:

- Salary after tax

- Side income

- Government payments (if applicable)

- Investment income (if applicable)

If you are self-employed, a simple starting point may be:

Net income = Gross income − Business expenses

You may also need to set aside funds for tax or other obligations depending on your circumstances.

Step 2: Assess your current spending

Track your spending for at least 30 days. You can do this using:

- Your banking app’s transaction categories

- A budgeting app

- A spreadsheet or notes app

Label each expense as:

- Need

- Want

- Savings or debt repayment

Then compare your current spending with the 50/30/20 guideline.

Step 3: Record your 50/30/20 split

Once you know your monthly income, calculate approximate dollar targets.

Example (monthly take-home income: $3,600)

- Needs (50%): $1,800

- Wants (30%): $1,080

- Savings/Debt (20%): $720

Some people find it easier to manage this by using separate bank accounts or budgeting “buckets”.

Step 4: Review your spending regularly

A simple routine might include:

- Checking spending once a week

- Reviewing category totals each month

- Adjusting your budget if certain categories consistently run over

Step 5: Automate savings where possible

Setting an automatic transfer into savings or a repayment account shortly after payday may help maintain consistency and reduce the need for manual budgeting decisions.

Step 6: Reassess periodically

Your budget may change due to rent increases, interest rate movements, family commitments, or income changes.

Reviewing your budget every few months can help keep it realistic.

Example of the 50/30/20 plan in action

If your monthly take-home income is $4,000, the guideline could look like this:

Needs (50%) = $2,000

- Rent: $1,500

- Groceries: $350

- Utilities: $100

- Transport: $50

Wants (30%) = $1,200

- Eating out and entertainment: $500

- Shopping: $300

- Subscriptions: $50

- Savings for holidays: $350

Savings and Debt (20%) = $800

- Emergency fund: $350

- Extra loan repayments: $200

- Investing: $250

This example is illustrative only. Your actual categories and amounts will depend on your household, location, and financial commitments.

When might the 50/30/20 rule not be the best saving strategy?

You may want to modify the framework if you are:

- Living in areas with high housing costs

- Carrying high-interest debt and focusing on repayment

- On a low income where essential costs exceed 50%

- Self-employed or working casually with irregular income

- Supporting dependents

- Working toward major goals such as a home deposit

- Living on a fixed retirement income

In these situations, the 50/30/20 rule can still be used as a reference point rather than a strict guideline.

Adjusting the 50/30/20 rule to your situation

You can customise the percentages to better reflect your circumstances.

Examples include:

- 60/20/20 if essential costs are higher

- 40/30/30 if you are prioritising savings or debt reduction

- 70/10/20 if most income currently goes toward essentials

Other adjustments may include:

- Budgeting from your minimum reliable income if earnings fluctuate

- Using higher-income months to boost savings or repay debt

- Creating sinking funds for irregular expenses such as insurance, school costs, or car registration

Tips for success with the 50/30/20 rule

- Compare utility providers where possible

- Cancel subscriptions you no longer use

- Plan meals to manage grocery spending

- Check eligibility for government rebates or concessions

- Look for free or low-cost entertainment options

- Use separate accounts for needs, wants, and savings

- Track spending through your banking app or budgeting tools

- Consider balancing debt reduction with building an emergency buffer

Managing unexpected expenses

Even with a structured budget, unexpected costs can occur. In these situations, people sometimes review options such as:

- Using emergency savings

- Adjusting discretionary spending temporarily

- Arranging payment plans with service providers

- Exploring support services or financial counselling

- Carefully comparing credit options offered by licensed providers where appropriate

If you are considering borrowing, it can help to:

- Understand the total cost of the credit (including fees and repayments)

- Check whether the repayment schedule fits within your budget

- Compare options and only borrow what you need

Credit24 is a licensed credit provider that offers personal loans between $500 and $10,000, subject to eligibility, lending criteria, fees and charges. Borrowing may not be suitable for everyone, so reviewing the terms and comparing options can help you make an informed decision.

Apply here:

https://www.credit24.com.au/au/apply/login

FAQ about the 50/30/20 budget rule

What counts as a need versus a want?

Needs are essential living costs such as housing, groceries, utilities, and transport. Wants are discretionary expenses such as entertainment, takeaway, shopping, or hobbies.

Should HECS/HELP repayments be included in needs or debt?

Because HECS/HELP repayments are typically compulsory and deducted from income, many people treat them as a “need”. Others classify them as debt repayments. Either approach can work if used consistently.

How should a windfall be handled in this budget?

Some people choose to allocate windfalls toward savings, debt reduction, and a smaller portion for discretionary spending. The exact allocation depends on your priorities and financial position.

What if my needs exceed 50% of my income?

This situation is common, particularly where housing costs are high. Adjusting the ratio (for example, 60/20/20) may help make the framework more realistic.

Can the rule work for self-employed income?

Yes, although it may help to calculate net income and allow a buffer for tax and income variability.

How can I budget with irregular income?

One approach is to base your budget on your minimum reliable monthly income and use higher-income months to increase savings or reduce debt.

Do superannuation contributions count in the 20%?

Employer super contributions are typically separate from take-home income, so they are usually not included. Voluntary contributions from after-tax income may be included if they fit within your savings plan.

How does the rule apply to shared household expenses?

Shared costs such as rent or utilities can be split between household members. Each person can then apply the wants and savings categories to their own income and goals.

Is it better to focus on debt repayment or savings?

Some people prioritise paying down higher-interest debt while maintaining a small emergency buffer. The right balance depends on interest rates, income stability, and financial goals.

Conclusion

The 50/30/20 rule is a simple budgeting framework that can help people better understand how their income is allocated between essential expenses, discretionary spending, and savings or debt reduction.

While it may not suit every household or income level, it can serve as a useful starting point for building budgeting habits and improving financial awareness.

Budgeting progress often comes from small, consistent improvements. Starting with a simple framework and adjusting it to reflect your real-world costs can help you build a system that works for your circumstances.

Disclaimer

IPF Digital Australia Pty Ltd, trading as Credit24, ABN 59 130 894 405. Australian Credit Licence 422839.

The information in this article is general in nature and does not consider your objectives, financial situation, or needs. Lending criteria, fees and charges apply. For product details, eligibility requirements, and full terms and conditions, visit www.credit24.com.au.

Start a loan application